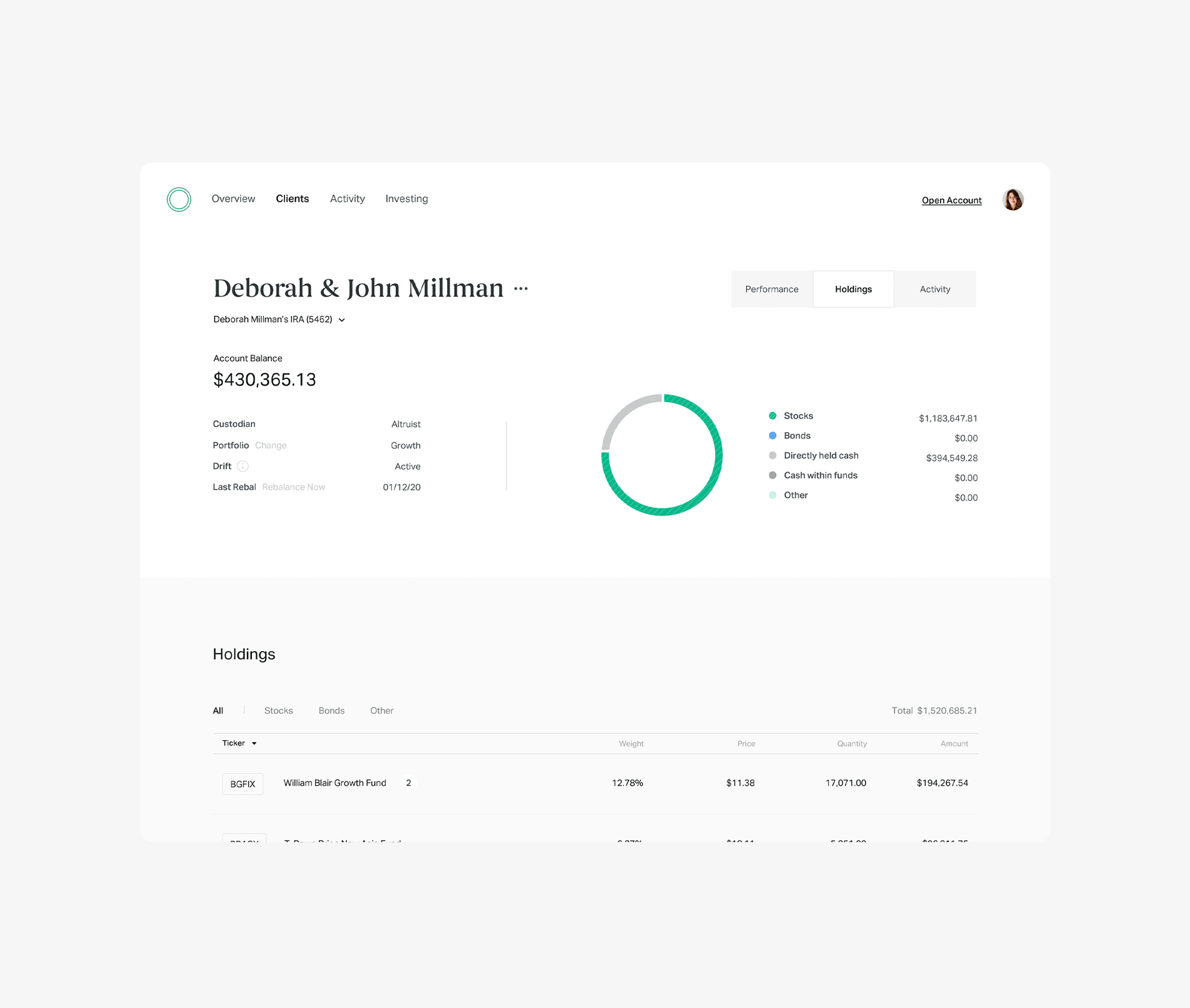

Here at Altruist, we're focused on developing tools to help financial advisors do their best work, including tools to make rebalancing simple and effective.

In building our rebalancing tool we’ve looked at two ways to automate rebalancing:

- Time-based rebalancing (monthly, quarterly, annually, etc)

- Threshold/drift-based rebalancing (relative drift from defined allocation percentage)

After speaking with advisors, doing web-based surveys, and researching other rebalancing tools, we’ve found the bulk of advisors are either not using a rebalancing tool, or are using a time-based rebalancing tool (with quarterly being the most frequent sequence).

However, in researching best practices to get clients maximum after-fee and after-tax returns, we discovered there is a smarter way to rebalance portfolios. And, it can be fully automated, freeing up advisors to work on other tasks while their client portfolios are monitored daily (but traded much less frequently).

Defining the Best Rebalancing Strategy

Many people think rebalancing can be used to either increase returns or lower risk (or both). This is only partially true. Rebalancing has only historically been effective in managing investment risk, but only marginally effective in increasing return.

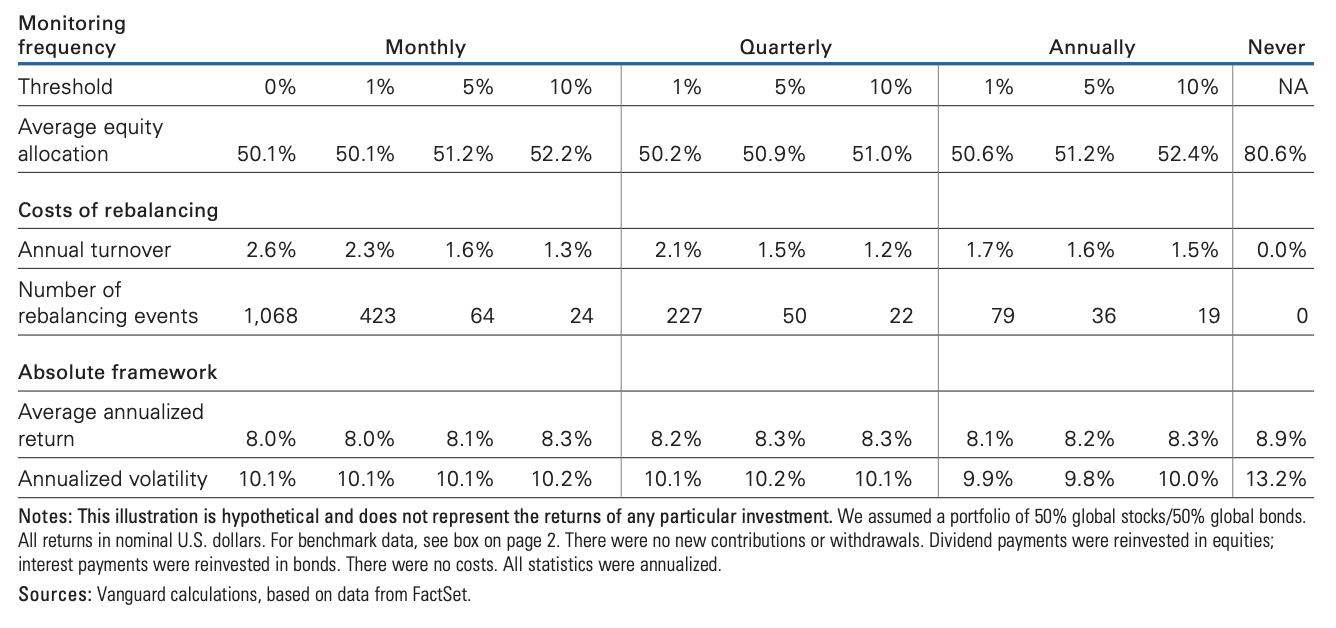

Vanguard published a paper in 2015 that showed the merits of using various rebalancing strategies from 1926 to 2015. Their findings showed gross returns are minimally affected by rebalancing. Risk, however, was managed well regardless of rebalancing methodology.

While the differences are small, the irony of the Vanguard study was that the ideal rebalancing strategy was with as large a threshold and as long a time sequence as possible. Using the above chart we can see that an annual time frame with a 10% threshold compared to a monthly time frame with a 0% threshold increases return by 0.3% while lowering the volatility by 0.1%.

The primary reason is by lengthening the rebalancing time frame and increasing the threshold we are harnessing the power of momentum in our investment strategy. In other words, we let our winners run a little longer.

There are other benefits too.

By increasing the time of frequency and increasing the threshold, we also trade less. This reduces investor costs as well as taxes (based on account individual client tax considerations).

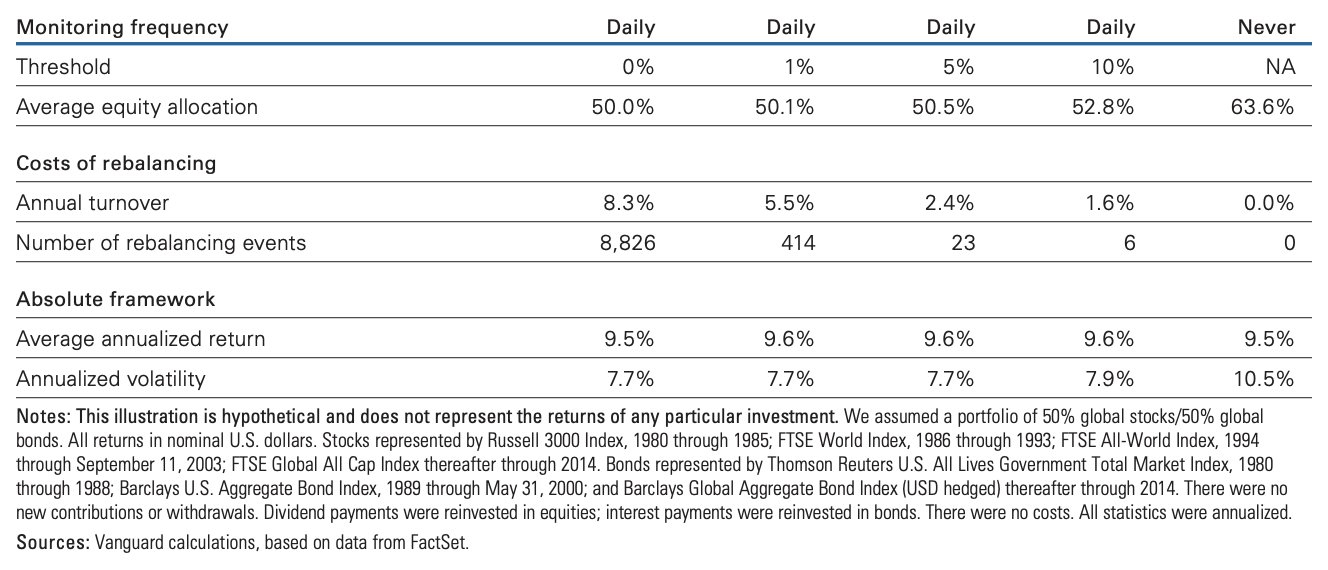

Vanguard didn’t have data going back to 1926 but did run a test using only threshold and no preset frequency from 1980 to 2015. The results of this study are below.

Automatic Rebalancing at Altruist

To help advisors achieve maximum efficiency while also delivering the best possible client experience, we’ve created a very simple model and portfolio trading system.

Advisors can create Models of any stocks, ETFs, and Mutual Funds on our platform. Models are managed on a percentage basis and there is no limit to the number of holdings per model.

Advisors can then create Portfolios of their models.

Finally, client accounts can be assigned to a portfolio.

Whenever you update a Model it will automatically trade only that model in each client account. Whenever you update a Portfolio all clients assigned to that Portfolio will automatically be rebalanced to your new Portfolio weightings.

When building a Portfolio you can choose “Automatic” or “Manual.”

Automatic has two settings:

- Our Passive setting has a drift setting of 25%. This means that your client portfolios will be monitored daily but only rebalanced if one of your models has drifted at least 25% from the target allocation.

For example, if you have a simple 50% SPY and 50% AGG portfolio, if either holding reaches 62.5% or 37.5% it would trigger a rebalance.

The benefit of this method is that you will have a lower cost, lower turnover, and most likely, less tax consequences. - Our Active setting has a drift setting of 15%. This means that your client portfolios will be monitored daily but only rebalanced if one of your models has drifted at least 15% from the target allocation.

For example, if you have a simple 50% SPY and 50% AGG portfolio, if either holding reaches 57.5% or 42.5% it would trigger a rebalance.

The benefit to this method is you will have better risk alignment, while still managing turnover and taxes reasonably well.

Manual gives you full control to choose the frequency of your rebalancing. This creates precise portfolio allocations on whatever time sequence you prefer, but will also trigger the largest amount of trades, and potentially the most adverse tax consequences.

In the end, we want to empower great advisors to do their best work. Building a simple, yet powerful rebalancing system is a big part of delivering on our mission.